The Seton Hall Health Sciences Campus, home to the College of Medical and Health Sciences and the College of Nursing, will receive $1.14 million in federal funding announced by Congressman Bill Pascrell (NJ-9), said the Senators Robert Menendez and Cory Booker.

Congressman Pascrell said, "I have visited the IHS campus many times, and each time I have been incredibly impressed with the teaching and learning that takes place there. We are delighted to have been able to secure much-needed funding for this valuable project. The Skills Healthcare Staff Will Gain in The Future of Lab Upgrade New Jerseyans have been in the 9th District and throughout NJ for decades.

Anticipating the continued growth in demand for medical education, Seton Hall requested funding to:

enhance the simulation lab experience;

Construction of control rooms.

simulation equipment

and simulation at the point of care.

The project will provide new equipment and enhancements to the Simulation Center on the IHS campus to ensure that nurses, occupational therapists, physician assistants, physical therapists, speech therapists, and sports trainers are clinically prepared to interact with real patients.

Catherine Sanuk, Coordinator of the Clinical Skills Laboratory, School of Nursing; With Jennifer McCarthy, Director of Clinical Simulations in the College of Health Sciences and Medicine; Preparation of financing proposal.

“The upgrades and equipment will enable the College of Nursing and the College of Health Sciences and Medicine to prepare future healthcare professionals to work in a patient-centered, integrated healthcare system, addressing healthcare shortages. and demand,” Sanuk and McCarthy noted.

Adds Joseph E. Nair, Ph.D., president of Seton Hall, "This achievement is the result of months of dedicated work by the faculty and staff of the College of Nursing and the College of Health and Medical Sciences, and our relationship with Seton Hall's management team and advocates in the nation's capital, such as Congressman Pasquerel and Senator Booker and Menendez, are grateful to each of them for their dedication to Seton Hall and the health of NJ.

For more business news, visitNJB News Now.

Related Posts:

Sixth Edition of the CMC Series with Seton Hall University: Your Guide to Running a Virtual Case Competition

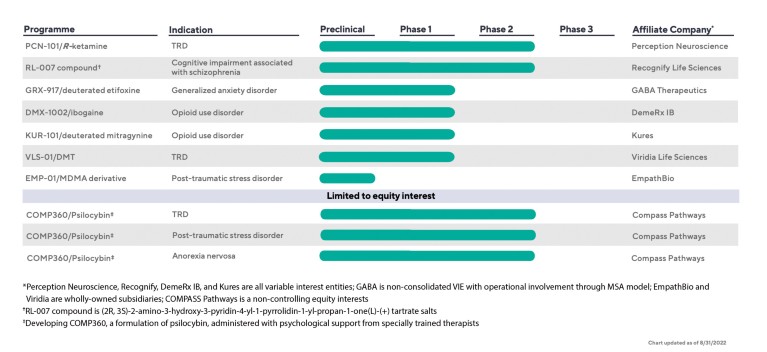

New York-based Perception Neuroscience, the clinical-stage psychedelic biotechnology company Atai Life Sciences (NASDAQ: ATAI ), announced the results of its PCN-101 study of a specific R-ketamine in patients with treatment-resistant depression (TRD).

Although the combination showed signs of efficacy at all time points, the study did not reach the primary endpoint of a statistically significant change from baseline in participants' MADRS (Montgomery-Asberg Depression Rating Scale) at 24 hours compared to placebo, the company said. The MRS is a widely used clinically assessed measure of depression severity.

A two-week trial study evaluated the safety, tolerability, and efficacy of a single intravenous injection of PCN-101 in 102 patients with TRD.

Other primary endpoints were the proportion of patients defined as responders, i.e. the proportion of patients with a 50% improvement from baseline on the MADRS and the proportion of patients with an overall MADRS score of less than 10.

Trending: Elon Musk says if Putin dies or is ousted, his successor in the UK will not be 'friendly' to the world

Should read : "Não nos pode jahil". Aki Estamos Nos' – Brock Pierce sobre or Blockchain Hub Davos 2023

For these measures, the study did not reach statistical significance, although response and remission rates were higher in the 60 mg group.

PCN-101 was generally well tolerated, with remission and withdrawal rates comparable to placebo.

Based on the overall results, Atai said it will look closely at the study data and work with understanding on next steps, "not limited to exploring strategic partnership options."

After this news, the share price of the company fell. Shares fell 30% to close at $1.86 per share.

Image: Benzinga via RODNAE Productions on Pixel and Doc James on Wikimedia Commons.

Gilead Sciences has pledged billions of dollars to Galapagos in an autoimmune disease partnership that is far from expected. But the drugmaker is not giving up on this therapeutic area and is now forming a new alliance with a new partner whose technology could offer treatments for rheumatoid arthritis and lupus.

The partner is EVOQ Therapeutics, a startup whose technology takes a novel approach to the antigen-specific immune response. Specific financial terms of the deal announced Tuesday were not disclosed, but the companies said EVOQ could receive up to $685.5 million in upfront payments, exercise options and milestone payments.

Autoimmune diseases develop when the balance of the immune system is shifted towards hyperactivation of immune cells. EVOQ's approach to treating such diseases targets dendritic cells, antigen-presenting cells that prime immune cells for immune tolerance or immune activation responses. The company says its technology can stimulate dendritic cells to trigger an anti-inflammatory response that restores immune tolerance.

The EVOQ technology, known as NanoDisc, is designed to deliver disease-specific antigens to lymph nodes, which are rich reservoirs of dendritic cells. Under the terms of the agreement with Gilead, both companies will collaborate on preclinical research. The agreement allows Gilead to license the NanoDisc technology exclusively for rheumatoid arthritis and lupus. If the Foster City, California-based drugmaker exercises those options, it will be responsible for the clinical development of drug candidates. If the drugs receive regulatory approval, Gilead will also market them. EVOQ will then receive royalties from sales of Gilead's commercial products.

"Despite great advances in the last two decades, there remains a significant unmet need for people with inflammatory and autoimmune diseases," said Flavius Martin, Gilead's executive vice president of research. "We are excited to partner with EVOQ to further expand our autoimmune line to meet the needs of people living with the condition."

Gilead expressed similar sentiments in 2019 when it reached a $5 billion deal with Galapagos to collaborate on six drugs in clinical phase and another 20 in preclinical development. The agreement expanded on a previous alliance for filgotinib, which was rejected by the FDA but received regulatory approval in Japan and Europe for the treatment of rheumatoid arthritis. Although Gilead collects royalties on sales of its partner's product, most of the drug is now owned by Galapagos. Other affiliate programs have also failed. In 2021, Gilead and Galapagos halted the development of giritaxate in idiopathic pulmonary fibrosis after an independent data monitoring committee evaluated the clinical data and concluded that the drug's benefits did not outweigh its risks.

Gilead is EVOQ's second pharmaceutical partner. Two years ago, the startup announced a secret licensing and collaboration agreement with Amgen to cover the development of new drugs for autoimmune diseases. The deal puts EVOQ in line for up to $240 million in initial and milestone payments.

Photo: David Paul Morris/Bloomberg via Getty Images

The clinical trial landscape in primary sclerosing cholangitis: current and new opportunities for patients

Nagpur, Jan 3 (PTI) Prime Minister Narendra Modi on Tuesday laid out his vision for science for the next 25 years, urging researchers to focus on making the nation self-sufficient and transforming their knowledge to make a difference in everyone's lives.

Inaugurating the 108th Indian Science Congress here, Modi emphasized strengthening scientific processes, focusing on new areas such as quantum technology, data science, developing new vaccines, strengthening efforts to monitor new diseases, and encouraging young people to do research.

“Science endeavors can become great accomplishments only when they leave the laboratory and reach the world, and their impact extends from the global to the grassroots level, from the journal to the ground (Earth, everyday life) and change is visible. From research. For real life," the prime minister said in a virtual address at the event.

The five-day Indian Science Congress kicked off at Rashtrasant Tukdoji Maharaj University in Nagpur in the presence of Maharashtra Governor Bhagat Singh Kashiari, Union Ministers Nitin Gadkari and Jitendra Singh, Chief Minister Eknath Shinde and Deputy Chief Minister Devendra Fadnavis.

The Prime Minister also took the important step of creating an institutional framework and teacher mentor system (guru shishi) that could build on successful talent hunts and hackathons to attract young people to science.

He highlighted opportunities for private companies and startups to connect with research labs and academic institutions. He urged researchers to focus on quantum computing and become world leaders in the future.

"India is moving fast towards quantum computing, chemistry, communications, sensors, cryptography and new materials," said Modi, urging young researchers and scientists to gain experience and become leaders in the quantum field.

The Prime Minister urged researchers to prioritize topics such as artificial intelligence, augmented and virtual reality and propose innovations in semiconductors.

"India is taking several initiatives in the semiconductor field. New innovations will be needed in the semiconductor field. Shouldn't we be thinking in this direction to shape the future of the country?" Dr Modi.

Addressing India's growing energy needs, he urged the scientific community to develop innovations that could benefit the country in this field.

Since India is home to 17-18 percent of the world's population, the development of so many people will also bring about global prosperity, he said.

India is leveraging science for progress and its impact is visible, he said, noting that India rose from 81st to 40th position in the 2015 Global Innovation Index out of 130 countries.

"Currently, we are living in a time when humanity is facing the threat of new diseases. We need to timely detect diseases through comprehensive disease control and take measures to fight them. Different ministries need to work together to achieve this." she says

Modi also stressed the importance of strengthening research and development to develop new vaccines.

Worst company in the world!! Blackstone and Blackrock

Gilead Sciences(NASDAQ:GILD) is one of the year's biggest stocks, up 17%, while the S&P 500 is down 21% over the same period. And the company may have given investors reason to remain optimistic about the stock. Health officials have given the go-ahead for another HIV treatment that promises to improve lives and generate billions in corporate revenue. Is it time to stockpile Gilead?

FDA approved lenacapavir

On December 22, Gilead Sciences issued a press release announcing that the Food and Drug Administration (FDA) had approved an HIV treatment, lenacapavir, to be marketed as Sunlenca. This treatment is approved for people with multidrug-resistant HIV. The six-monthly injection will give many HIV patients a longer option than the daily pill they are currently on. Importantly, it is not approved for everyone with HIV, only for those "who cannot be successfully treated with other available therapies because of resistance, intolerance or safety concerns."

For investors, this is as important a win as success for Gilead. Analysts estimate that lenacapavir could generate $1.5 billion in revenue at its peak. This will represent approximately 5.5% of the $27 trillion in product sales reported by Gilead last year.

In terms of value for money, it may not be a game changer, but it's still a significant accomplishment for Gilead. CEO Daniel O'Day said, “Gilead scientists have developed the unique and powerful antiretroviral drug Sunlenca with flexible dosing options. Our goal is to provide multiple long-term care options.

Gilead is actually positioning itself to be in the best position to capitalize on the growing need for HIV care. Fortune Business Insights estimates that the global HIV drug market will be valued at over $45 trillion by 2028, and a compound annual growth rate of 5.9% until then.

Gilead could use a growth catalyst

One of Gilead's recent challenges has been finding ways to ensure sustainable growth, and Sunlenca can help. Over the past three quarters, Gilead's revenue excluding the COVID-19 drug Vecluri was $16.7 billion, up just 7% year-over-year. And the growth rate of its largest segment, HIV, is even lower, at just 5%. Therefore, Sunlenca's agreement gives investors an opportunity to bounce back and be able to generate even stronger growth in the future.

The stock is currently trading at multiples of 13 (less than the health average of 17), indicating that investors are a little wary of the company and unsure of its upside potential. Gilead stock has yet to receive FDA approval, but the stock likely has lost money in recent months, thanks in part to strong earnings reports and generally favorable market growth prospects for the stock. While this is a big win for the company, the backing may not be enough (financially) to push the stock higher than before.

Is Gilead Sciences a Share Buyback?

Gilead Sciences has a strong HIV business that recently got another opportunity with support from Sunlenca. Despite increasing value, Gilead shares are not overvalued and are still a bargain. And with a dividend yield of 3.5%, there's even an added incentive to buy and own medical stocks because they are an investment that can be a good source of regular cash flow for your portfolio.

Sponsors:

10 stocks we like better than Gilead Sciences

When our award-winning team of analysts has valuable advice, it's worth listening. After all, the Motley Stock Advisor newsletter, which has been around for over a decade, has doubled the market*.

Investors just named ten stocks they believe are the best buys right now… and Gilead Sciences isn't one of them! That's right: they think those 10 stocks are a better buy.

View 10 promotions

* Exchange Advisor returns on December 1, 2022.

David Jagielski was not interested in this action. Motley Fool has and recommends positions at Gilead Sciences. Motley Fool has a disclosure policy.

Shares of Guardian Health Sciences Inc. (NASDAQ: GHSI ) rose on Friday 12/30/22 as the stock price rose 0.76% from the previous day's close as strong buying pushed the stock up $0.15.

Actively tracking price action in recent trades, the stock closed the session at $0.14, reaching a range of $0.142 to $0.151. The beta value (monthly after 5 years) was 0.85. Referring to the stock's 52-week performance, the high was $0.74 and the low was $0.13. Overall, the GHSI changed by -15.88% over the past month.

5 Undervalued Stocks for 2023

About 544 miles north of Las Vegas is what has been described as "the largest lithium deposit in the United States." Small businesses will benefit greatly as lithium "faces a long-term supply shortage," Barron's said. However, this company has a gold mining opportunity as it plans to produce 30,000 tonnes per year over the next 3.5 years from this unique deposit. Fueling the electric car boom and possibly sending their stock prices off the charts. But that's just one of the possibilities we've explored in our free report. The remaining four companies have the same potential.

Click here to download your free copy…

Sponsorship

As the market capitalization of Guardian Health Sciences Inc. currently stands at around $9.21M, investors are looking forward to the results for this quarter which is expected from March 30, 2023 to April 3, 2023. Therefore, investors may wish for the stock to increase in value. before the company releases its earnings report. Analysts expect the company's earnings per share (EPS) to be $-0.03, which is expected to decrease to $-0.05 in FY-0.15 and then to around $-0.13 by FY2023. year.

Analysts estimated the company’s revenue for the quarter at $2.95 million, with a low estimate of $2.7 million and a high estimate of $3.2 million.

Reviews can be a useful indicator for understanding short-term price movements; therefore, there have been no bullish or bearish changes over the past seven days. We can see the technical chart of the GHSI, which shows that the short-term indicators are showing that the stock is selling at an average of 50%. However, medium-term indicators place the stock in the Hold category, while long-term indicators put the stock at 100% on average.

1 analyst(s) rated their futures rating on the stock on a scale of 1.00 to 5.00, indicating a strong buy or sell recommendation. The stock has 0 analyst hold ratings, 1 buy rating and 0 GHSI Stock Overweight ratings. Meanwhile, 0 analysts think the stock is underweight and 0 think it is a sell. Therefore, investors who want to increase their stake in the company's shares will have the opportunity to do so, as the average rating of the stock is a buy.

Technical analysis of the stock shows that PEG ratio is close to zero and GHSI price is currently trading close to -9.88% and -10.33% from its 20 and 50 day simple moving averages respectively. The Relative Strength Index (RSI, 14) is currently at 40.71, and the 7-day volatility report shows 6.71%, or 9.40% on the 30-day chart. Also, Guardian Health Sciences Inc.'s beta value. (GHSI) is 0.88 and its Average True Range (ATR) is 0.01. The company's stock price is expected to average $0.60 over the next 52 weeks, with a low of $0.60 and a high of $0.60. Based on these price targets, the low is -300.0% of the current price, while the price is expected to move -300.0% to the high of the year. Additionally, investors should welcome the analyst average price of $0.60 as it represents a -300.0% downside from current levels.

Historical trading data from Guardian Health Sciences Inc. (NASDAQ:GHSI) shows an average trading volume of 0.57 million shares over the past 10 days and 1.09 million shares over the past 3 months.

About 1.34% of Guardian Health Sciences Inc. owned by insiders, while institutional investors own 7.70% of the company's shares. The short interest data also shows that there were 5.43 million shares shorted as of December 14, 2022, corresponding to a short put ratio of 6.86. According to the data, a low stake in Guardian Health Sciences Inc. (GHSI) was 8.82% of shares outstanding as of December 14, 2022; the number of short shares recorded on November 14, 2022 reached 5.57 million. The stock is down 77.58% year-to-date, indicating further upside potential. This could boost investors' confidence that they are bullish on GHSI stock next quarter.

GUARDION HEALTH SCIENCES INC AWARDS FOR YOU | GHSI BUCKS ANALYSIS | GHSI BUCKS FORECAST

Achieve life sciences, miss income expectations. EPS came in at $1.35 per share compared to the expected $1.13 per share.

Operator : Ladies and gentlemen, good afternoon, and welcome to the Life Sciences Third Quarter 2022 Revenue Call. All lines have been converted to Listen Only mode. The forum will be open for questions and comments after the presentation. In the meantime, I’d like to turn the floor over to your host, Nicole Jones, Investor Relations Specialist at CG Capital. Madam, you have the floor.

Photo by Yulia Koblitz on Unsplash

NICOLE JONES: Thanks operator. In today’s conversation with Axeve, John Bencic, CEO; and chief accountant Jerry Wang. After the prepared comments, Success Management will be available for questions and answers. I would like to remind everyone that today’s call contains forward-looking statements that are based on current expectations. These statements are only projections and actual results may differ from those anticipated. Please refer to Achieve’s SEC filings which may affect the company. I will now hand over to John.

John Bencic: Thank you, Nicole, and thank you to everyone who joined us today. Once again, the success quarter was a busy and exciting one. As we continue to push cytocycline through the clinic, we are poised to become the first new treatment for nicotine addiction in nearly two decades. In September, we announced the completion of targeted recruitment of participants for our Phase III ORCA-3 confirmation study on smoking cessation. And just last week, we announced that the Phase II trial of ORCA-V1 for nicotine e-cigarettes, or smoking cessation, completed better than expected. Of note, the ORCA-3 trial is the second and final phase III randomized trial that requires FDA submission and potential marketing authorization in the United States.

The design replicates the experience of the previous ORCA-2, which yielded excellent results earlier this year. Both trials were designed to evaluate the efficacy, safety, and tolerability of cytocycline 3 mg. The trials share the same primary endpoint for smoking cessation in the past 4 weeks, which is the primary endpoint for FDA-approved smoking cessation medications. The ORCA-2 results, if confirmed, would further solidify our belief that cyclicine could become the new gold standard in the treatment of nicotine addiction. Given the unequivocal incidence of side effects, the side effect profile of cycline is better than that of currently available therapies.

In terms of effectiveness, the odds ratio we observed with ORCA-2 at the end of treatment was six to eight times higher than placebo. Moreover, despite the high participation of the research team and the effectiveness of the trials during the outbreak, our dropout rate was extraordinary. We look forward to seeing similar results from ORCA-3 and look forward to sharing them with you in the second quarter of 2023. Vaping remains an important topic worldwide, especially given the alarming number of teens using it and the new evidence of harmful effects Potential on the cardiovascular system and respiratory system. More than 2.5 million middle and high school students in the United States alone use e-cigarettes, according to data released by the Center for Disease Control (CDC) last week.

More than 11 million adults in the United States use nicotine, and there is currently no approved treatment for smoking cessation. We initiated the ORCA-V1 trial expecting the steady cycle to be of benefit to this growing and overexerted population. The rapid recruitment of ORCA-V1 supports our hypothesis of a therapeutic need in this population. The target recruitment of 150 ORCA-V1 subjects was completed within four months, with recruitment completed at only five clinical trial sites. By design, ORCA-V1 will evaluate a 12-week course of citiccycline versus placebo. As with other ORCA studies, all participants will receive behavioral support during the study. The primary objective will be to assess successful nicotine withdrawal, defined as weekly abstinence from sex over the past 4 weeks, with cotinine levels as a biochemical evidence of abstinence.

ORCA-V1 data is expected to be available in the second quarter of 2023. After two test cases, we will focus on three main issues in the coming months. First, ongoing communication with the ORCA-3 and ORCA-V1 clinical trial centers and third-party clinical research organization to ensure data is accurate and timely. Second, careful preparation for the US NDA implementation, including successful results from the ORCA-3 trials, and completion of the remaining additional trials required for the application. Third, commercial readiness, including initiating preparatory activities and discussing partnerships with stakeholders with the greatest potential for citcycline.

We also continue to work closely with our manufacturing partner Sofarma to ensure there is sufficient commercial potential at launch as part of our commercial readiness objective. As we announced today, Sopharma recently invested over €3 million to complete construction of a new cytocycline API purification facility and main production facility in Sofia. The new API package complements Sopharma’s annual production of nearly three billion tablets. Now I’d like to take Jerry’s call regarding our third quarter financial results.

Also see Top 10 Widows and Orphans Stock Returns and Jim Cramer Stock Returns.

Jerry Wang : Thank you, John. I will provide an update on our cash position as of September 30, 2022 and review our operating expenses for the third quarter. As of September 30, 2022, cash and cash equivalents, short-term investments, and restricted cash were $18.2 million compared to $43 million as at December 31, 2021. Our financial projections include a $2.5 million grant from the National Institutes of Health. Supporting the ORCA-V1 phase II study to evaluate the use of cetirizine as a nicotine stopping agent for e-cigarettes. Of note, about half of the ORCA-V1 trials are funded by a grant from the National Institutes of Health. According to the income statement, net loss for the quarter ended September 30, 2022 increased to $13.1 million from $6.7 million for the same quarter of 2021.

For the nine months ended September 30, 2022, net loss increased to $31.1 million, compared to $26 million for the same period in 2021. Operating expenses increased in the third quarter due to the testing and operation of ORCA-3 and the achievement of planned acceptance. In our experience ORCA-V1. We expect our quarterly operating expenses to be higher in the fourth quarter of this year and then decrease in the first half of 2023 after the completion of the ORCA-3 and ORCA-V1 trials. This concludes my financial comment. I will now hand over to John.

John Bencic: Thank you, Jerry. 2022 is critical to success, with key milestones being the results of the Phase 3 trial and the completion of enrollments in two other major studies. We are excited to continue advancing our process and are committed to advancing this important new treatment. Cigarette and nicotine addiction directly affects more than 1 billion people worldwide. In the United States alone, more than 30 million people smoke cigarettes, and about 0.5 million people die from smoking-related diseases. According to the analysis, 80% of new smokers who want to quit smoking are interested in new smoking products.

We think it would be better for Cytocycline in the class, 93% of them want something new. Existing treatments are very troublesome for smokers and addicts alike, and new options are long overdue. Much more needs to be done to help people who want to quit smoking improve and extend their lives. At Cytocycline, we believe we have a unique opportunity and responsibility to make a real difference. Thanks again everyone for your continued support and for joining us today. Now I would like to transfer the call to the operator and open the line for questions.

Click here to continue reading the Q&A session.

King 2022 distributed the full list of 37 companies

Alimera Sciences (NASDAQ:ALIM) had sales of $1,360,000 during the third quarter, according to Benzinga Pro . Profit fell to $5.26 million, down 68.76% from last quarter. In the second quarter, Alimera Sciences posted revenue of $1,460,000, but lost $3,120,000 in profit.

What is growing?

Return on invested capital is a measure of a firm's annual gross profit on invested capital. Changes in revenue and sales indicate changes in a company's ROCE. A higher ROCE usually indicates successful company growth and is a sign of higher earnings per share in the future. A low or negative ROCE indicates the opposite. Alimera Sciences reported a ROCE of 0.29% in the third quarter.

Note that although ROCE is a good measure of a company's recent performance, it is not a reliable predictor of a company's profits or sales in the near future.

Trend: Bill Gates says it could lead to civil war and 'end everything'

Must Read: Is Mister Beast Elon Musk Sensitizing The Platform As Twitter CEO 'Not Out Of The Box'?

ROCE is a powerful indicator for comparing capital allocation efficiency for similar companies. A relatively high ROCE indicates that Alimera Sciences can operate at a higher efficiency than other companies in its industry. If a company earns a high return on its current level of capital, some of that money can be reinvested in additional capital, which usually results in higher returns and ultimately higher earnings per share (EPS).

For Alimera Sciences, positive ROI of 0.29% indicates that management is deploying its capital effectively. Effective capital allocation is a positive indicator that a business will achieve long-term success and favorable long-term profitability.

Analysts forecast

Alimera Sciences reported Q3 EPS of -$0.75 per share, missing analysts' expectations of -$0.4 per share.

This article was generated using Benzinga's automated content engine and reviewed by an editor.

Danbury, Western Connecticut State University's Senate overwhelmingly rejected the university's current president's proposal to eliminate four social science graduate programs, but opponents worry the plan isn't dead.

Faculty and students protested plans by university officials to scrap major courses in economics, social sciences, meteorology, anthropology and sociology.

The Senate this week rejected all four major proposed cuts; in economics by 21 votes to 4; in anthropology and sociology – 20 votes "for" and 4 "against"; in social sciences – 19 votes "for" and 4 "against"; In Meteorology, the score was 21:2. Now President-elect Paul Beran must decide whether to follow the Senate's advice or advise the Board of Trustees to eliminate the seniors.

Monday's vote comes at the end of a 60-day period that allows interested parties to publicly testify and argue their position on keeping or eliminating large companies.

Public testimony ends Wednesday, but a university spokeswoman said Beran's decisions likely won't be made "for some time."

"During the joint governance process, there have been many discussions that have presented alternatives to the original proposal and we will continue to discuss them with the relevant parties," Beran said on Tuesday.

Rotua Lumbantobing, professor of economics and president of the WSCU chapter of the Association of American University Professors, is one of many professors who oppose the proposal to eliminate graduate programs.

He pointed out that the decision made by the members of the senate on Beran's last proposal is rejected and will be submitted to the Council of Regions for final approval.

"This process was rigged from the beginning," Lumbantobing said after the vote, adding that she and other teachers don't expect Bera to change his mind.

Lumbantobing added: "He has received an order from the Governing Council, so we expect it to be implemented."

The state Board of Regents, the body responsible for overseeing Connecticut's public higher education system, hired Berra over the summer to replace John Clark, who was voted out of confidence by disaffected faculty members in June. Reserve funds have been 99 percent depleted, in addition to other "severe" financial problems identified in a report earlier this year.

The report from the National Center for Higher Education Management Systems calls, among other things, for the university to review its curriculum and programs. This includes assessing whether you can continue to supply all low-grade items.

Byrne, who has spent his career managing state universities such as Arkansas, Oklahoma and South Dakota, told the News-Times in August that he was hired by WCSU to handle financial issues and discuss a "black and white new" school. Budget. Off" ".red" to report.

A university spokeswoman said an analysis of enrollment and retention trends data showed a drop in enrollment and less interest in the social science courses it proposed to exclude, but courses in all disciplines were still declining. – Students and college students.

After the move, there will be no teacher cuts, and students currently enrolled in major programs will complete their studies and receive degrees.

According to the university, WCSU currently has 22 economics majors, 19 anthropology and sociology majors, 10 social science majors, approximately 42 political science majors and 34 meteorology majors. In the year In 2017, the university reported awarding 22 undergraduate degrees in anthropology/sociology, 21 undergraduate degrees in business administration, 47 undergraduate degrees in political science, 26 undergraduate degrees in social science, and 34 undergraduate degrees in meteorology.

When Bera submits a proposal in its current form or revised form, the National Research Council Committee reviews it and the Regency Council decides whether to approve or reject the recommendations.

Lumbantobing admitted that she and other faculty members were not hopeful graduate programs would be supported, but said the rally was planned for the Feb. 3 board of trustees meeting.

"All public universities and community colleges are in short supply, which suggests that the state should either give us funding or give us more money, especially when it comes to declining enrollment," he said.

An evening of conversation with Dr. Yuval Levin et al. William Galston, by Dr. Daniel Barrett.

Gilead Sciences(NASDAQ: GILD) is a leading healthcare company that derives the majority of its sales from drugs used to treat HIV. And he has an exciting new treatment, lenacapavir, that, if approved by the authorities, could be a game changer for HIV patients and drive significant growth for Gilead.

Given the stability the company offers investors, strong earnings, and attractive growth prospects, it's no wonder the stock has performed so well this year, up more than 20% so far. But given that the stock is now trading near a 52-week high, is Gilead still a good buy?

Lenacapavir news could push stocks higher

Lenacapavir is an HIV treatment that only requires patients to receive one injection twice a year. This is a significant change from the daily pill that many HIV patients take today. While injectable medications may be less desirable than oral medications, the frequency with which patients must administer them can make them a much-needed option.

At its peak, lenacapavir could generate more than $4 billion in sales. This would make it one of the company's best-selling drugs. Last year, only Biktarvy, another HIV drug (a daily pill), made more money, with sales of over $8.6 billion. The Food and Drug Administration accepted Gilead's new application for the drug lenacapavir earlier this year and scheduled the PDUFA for Dec. 27, meaning a decision on treatment should be made soon.

This positive news front could easily propel Gilead stock to new highs as it would open up huge growth opportunities for the company. And the company recently announced strong results.

The latest results are better than they look

In its third-quarter earnings report (for the period ended Sept. 30), Gilead's revenue disappointed by more than $7 billion and fell 5% year over year. But excluding the COVID-19 treatment, Veklury's sales rose 11%. Many industries are showing impressive growth.

Trodelvy Cancer Care, which is still in the early stages of growth, had revenue of $180 million for the quarter, up 78% from the same period last year. Gilead's cell therapy product sales rose 79% to $398 million, and sales of its hepatitis C drugs rose 22% to $524 million. Its core HIV business also generated revenue of $4.5 billion, up 7% year over year.

Gilead's business has been strong lately, and while expenses rose last quarter, primarily due to contract-related R&D costs (a one-time fee from a recent acquisition), the company's margins and operating practices have surprisingly improved . %. Revenues.

Investors also receive strong dividends

Gilead is also a good returnee. It gained 3.3%, nearly double the S&P 500 average of 1.7%.

The company has increased its payouts over the years, with the current quarterly dividend of $0.73 being higher than the $0.52 Gilead paid five years ago. And with Gilead's trailing-12-month free cash flow of $9 billion, Gilead is in a good position to keep increasing its payout, which has cost the company $3.7 billion over the trailing 12 months. Gilead's earnings don't appear to be in jeopardy, and this is a boost investors can count on for the foreseeable future.

Gilead is still a good buy today

At 34 times earnings, Gilead stock looks expensive (the healthcare industry average is 23), but it's also high as the company's recent earnings report, which said research and development costs have risen, weighs on earnings Has. Based on analyst forecasts, Gilead is trading at a multiple of 13 times future earnings, down from the industry average of 17.

Although Gilead has appreciated in value, it's still an investment that offers investors a lot of value and could be a great stock to own in 2023. Given its earnings, the company's growth, and the potential that lenacapavir has to offer, the stock could be a solid and profitable dividend for your portfolio for years to come. .

Sponsors:

The 10 Stocks We Love Most at Gilead Sciences

When our award-winning team of analysts have stock advice, it's worth hearing about. After all, the newsletter she's been publishing for more than a decade, The Motley Fool Stock Advisory , has tripled the market. *

They just revealed what they think are the 10 biggest stocks investors can buy right now… and Gilead Sciences isn't one of them! It's true: You think these 10 stocks are a better buy.

Show 10 titles

*The Portfolio Advisor will come into effect again on December 1, 2022

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has a mission and recommends Gilead Sciences. The Motley Fool has a disclosure policy.

Great Opportunities for Gilead Sciences | Gold stock news