George Santos made major revisions to his campaign finances on Tuesday, according to The Daily Beast.

Redacted documents show that a $500,000 "personal" loan for his 2022 campaign was not personally financed.

Experts say the tampered files add to the mystery of Santos' dubious balance sheets.

Thank you for your registration!

Include your favorite topics in a personal stream wherever you are.

Rep. Jorge Santos' political process made significant changes to his 2022 campaign documents on Tuesday, The Daily Beast reported, revealing that a $500,000 "personal" loan he made to his campaign in March did not come from his own money not.

The initial deposit showed that the "candidate's personal funds" box was checked when the campaign Mega Loan was entered, while the amended deposit left the box blank.

The revised deposit does not indicate the source of the funds, or if there are guarantees for the loan, much of the entry is left blank.

Another filing filed Tuesday revealed that none of the $125,000 loan the candidate made to the Santos campaign in October came from his personal funds.

Ever since Santos was criticized in the media for lying about key elements of his life, there have been questions about the six-figure sum he said he lent to his campaign.

He donated $705,000 of his own money to his last successful 2022 campaign, far more than the $55,000 he reportedly received when he ran for Congress in 2020.

Brendan Fisher, deputy executive director for government oversight and campaign finance expert, told The Beast the amended documents do little to resolve unanswered questions about funding.

"If the candidate's loan did not come from the candidate, Santos should have explained where the money actually came from," Fisher told The Beast.

"Santos cannot untick the box and get rid of his legal problems," he added.

Campaign finance experts told The New York Times that the redacted documents only add to the opacity of Santos' financial information.

"I've never been more confused about reviewing an FEC filing," Jordan Liebowitz, a spokesman for Citizens for Responsibility and Ethics in Washington, told the Times in an interview.

Brett J. Capel, an election finance and ethics attorney, told the Times that the tampered files raise the possibility of lawlessness.

"If the candidate's personal wealth was not the source of the loan, what was?" He said "The only other source is the bank, and they will require collateral for a loan of this size. If the bank is not the source of the funds, the only alternatives are illegal sources."

In a WBAC radio interview last month, Santos insisted the campaign contributions were legal.

He said he paid the money himself through his company, the Devolder organisation, and told Semaphore he did "specialist advice" for "highly advantaged individuals".

Appearing on the conservative "Bannon's War Room" podcast earlier this month, Santos avoided describing the source of the loans, telling Rep. Matt Gaetz said: "I will tell you where they do not come from. Are they from China or China. Ukraine or Burisma ".

The Daily Beast's report led Democratic Representatives Richie Torres and Ted Liu to call for Santos' resignation or impeachment, with the latter accusing the Republican representative of a crime.

Earlier this month, Rep. James Comer, the new chairman of the House Oversight and Accountability Committee, said Santos would be expelled from Congress if he was found to have violated campaign finance laws.

Santos' finances and schemes are now being investigated by federal prosecutors in New York state and Brazil.

Santos did not immediately respond to Insider's request for comment.

The upcoming 2023 federal budget will be a key way to determine whether the NDP's confidence and supply deal with the Liberals has been a success or a failure, according to the party's tax critic.

"I think the budget will show whether we're on a good pace or not," NDP MP Danielle Blakey told the CBC. "It's going to be a very interesting few months here on the Hill … when the budget comes down."

In March 2022, the New Democrats signed an agreement with the governing Liberals to secure the votes needed to pass major legislation if the Liberals agreed to advance some of the MDP's priorities. That deal will be a big talking point as Blakey and his 24 NDP colleagues attend a rally on Parliament Hill starting Wednesday.

New Democratic Party leader Jagmeet Singh will kick off the morning with a press conference. He promises to address issues such as health care and the inflation crisis. The rest of the meeting will be closed.

In closed sessions, Blakey will update his colleagues on ongoing discussions with the federal government as part of a bipartisan group of policymakers and staff formed after the signing of the agreement to discuss progress on key commitments and priorities. .

Expansion of the pharmacy and dentistry plan on the MDP radar

Although many of these priorities do not have deadlines, some do.

For example, 2023 was supposed to be the year the Liberals passed the Canada Medicines Act, and then a procurement plan and a national formulary or essential drug list would follow until the OK expires.

In 2022, dental coverage was expanded to include children up to age 12 in families earning less than $90,000. Expanding dental coverage for middle-income families to 18-year-olds, seniors and people with disabilities would take another step this year under the deal.

The New Democrats will scrutinize Finance Minister Chrystia Freeland's spring budget to see if the Liberals are serious about sticking to the rest of the deal, according to the finance critic.

Blakey noted that since most budget preparations are done months in advance, the 2022 budget was largely developed before the confidence and supply agreement was signed. That's why he says the next budget will "say a lot" about what the NDP-Liberal deal looks like.

"It will be an important moment of reflection for our team as we think about next year and whether the government is doing a good enough job."

PKD will protect the public health system

Along with promoting various aspects of the deal, Blakey said the New Democrats will push the Liberals to fix the health care system.

He said Canadians "are seeing their health care system fail at a time when they need it most."

Ontario's Progressive Conservative government announced plans Monday to increase the number and choice of surgeries offered at not-for-profit clinics across the province.

After the announcement, Prime Minister Justin Trudeau said he was open to "providing better health services for Canadians."

Meanwhile, Ontario and the federal New Democrats have left no doubt about the party's stance on a private system on public funds, saying parallel systems would create competition for scarce human resources.

"The ADP government is going to go against the provinces on private deliveries and we're watching that closely," Blakey said.

"We are unequivocal in our message to government that protecting public service offerings must be a priority for the federal government."

Blakey called on the federal government to use the "leverage" at its disposal to find solutions against conservative provincial governments that may target private health facilities.

A health workforce strategy is needed. Work group

What Canada needs is a national strategy for health workers, according to the country's largest labor organization with close ties to the PHD.

Bea Bruske, president of the Canadian Labor Congress, said the strategy would help Canadian governments recruit, train and retain health workers.

"Our public system is in trouble and we are calling on all levels of government to work together to ensure that Canadians across this country have strong public health care," said Brusk, who will also addresses the NDP caucus on Wednesday. . .

French federal leaders debate 2019 (English translation) Part 1

The outlook for the global economy in 2023 is "bleak", says the World Economic Forum.

A survey of economists published on the opening day of Davos shows that the risk of a global recession is increasing.

According to a World Economic Forum report published on the opening day of Davos: Leading economists' forecast for the global economy in 2023 is "bleak", with weak growth and a recession expected.

The World Economic Forum's Leading Economists' Outlook for January 2023 summarizes the views of some of the leading economists.

"Despite reasons for optimism, such as easing inflation, some aspects of the outlook remain bleak," the report said, citing "continued economic uncertainty and political challenges of historic proportions."

Almost two-thirds of the 22 leading economists surveyed by the WEF think a global recession is likely by 2023, with 18% saying it is "very likely".

"The prospects for global growth have weakened and the risks of a global recession are high," the report said.

But respondents to a panel of experts from financial and business firms such as UBS, Google, Microsoft and Bank of America expected to see big regional changes in economic growth next year.

All economists said they expected weak or very weak growth in Europe, 91% said they expected growth in the US, less than half in the Middle East, North Africa, South Asia, China and East Asia and the Pacific Ocean. . . More than half of respondents said they expect high inflation in Europe, only 5% in China.

This reflects high energy prices, interest rates and "cooling demand" in Europe, the WEF said. In contrast, China's reversal of its zero-transmission policy for Covid-19 could slowly boost the country's economy, although it could halt production if more people contract the virus.

Companies including Amazon, Goldman Sachs and Salesforce have announced layoffs this year, and leading economists expect layoffs to continue. 86% of respondents said multinational companies will reduce operating costs and 78% expect reductions. Most economists say companies expect customers to pay more.

But despite the largely pessimistic outlook, the report points out that some of the world's economic woes may ease this year.

Two-thirds of respondents said they expect the cost-of-living crisis to ease by the end of 2023, while nearly two-thirds expect the energy crisis to end by 2023. They said they hope to start making improvements by at the end of 2023. But Dimon predicted in December that Europe's energy crisis would worsen and possibly last for years.

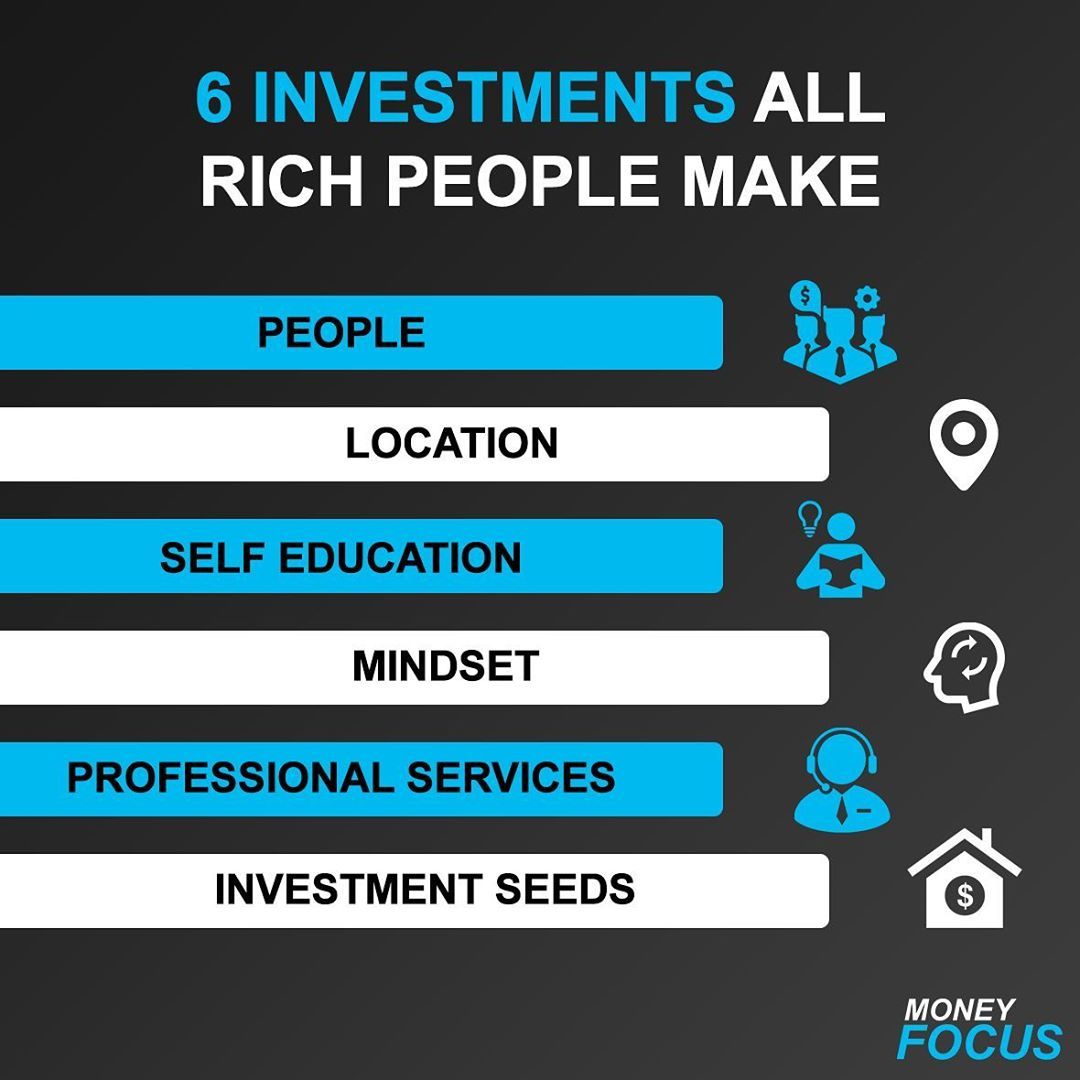

"This is the biggest secret of the rich" – Dr. John Demartini

Innovative blended finance models are key to attracting the private capital needed to help low-income countries mitigate climate change.

Recent Fair Transition Partnership Agreements with South Africa, Indonesia, and Vietnam highlight what is needed.

The International Monetary Fund says the world needs to spend between $3 and $6 trillion a year on mitigation by 2050.

Net-Zero Asset Owners Alliance, Owners of $10 Trillion, Says Lower Risk Will Help Them Invest

Climate finance partnership with BlackRock has raised $673 million with a focus on energy storage and renewables.

January 13 – There is a huge black hole in the funding needed for the climate and energy transition.

Currently, the costs (mainly for mitigation) are around $600 billion. Africa alone needs $3 trillion by 2030, and the world needs $3-6 trillion annually by 2050, according to the International Monetary Fund. That sounds like a lot, but private investors have money: They control $210 trillion worth of assets; Banks have the potential for an additional $200 trillion. How do you convince them to spend some of it?

The answer depends on the risk. Low- and middle-income countries are a risky proposition for investors, said Chris Klopp, CEO of Convergence Finance, a non-profit organization set up to increase investment in these countries to achieve the Sustainable Development Goals. Country and currency risks are so high that if investors invest, they will violate their fiduciary obligations to pension fund holders, shareholders and stakeholders or fail to comply with regulations.

But the appetite is there, says Clubb, if the risk is reduced enough to push him over the barrier. This is where blended financing comes into play: the use of public sector financing to reduce the level of risk to something acceptable to private investors.

Groups like the UN-backed Net Zero Asset Owners Alliance, which manages $10 trillion in assets, "say three things: First, we have money we want to invest. Second, we've seen developing countries and we want to invest money there, but the risks too high for us.” And third, if you can make a credit investment through mixed finance, we will invest.”

Mixed finance is not a new idea, but since the launch of the UN's Sustainable Development Goals (SDGs) in 2015, it hasn't worked out as expected. "We don't stick together on size. We mix small projects. So we have to break the glass to get more moving," said Guy Collins, vice president of banking, capital markets and trading at Citigroup. Council, at a side event at COP27 in November.

Convergence has tracked more than 700 mixed financial transactions over the past 15 years. Too often, says Klopp, only one donor government provides the money, limiting the size of the mix of financing instruments. On average, these transactions amount to around $70 million, which is quite a small amount for a change of scenery.

Bringing governments, multilateral development banks and the private sector together could change that. An example is the climate finance partnership announced at COP26 by asset manager BlackRock.

Focus on renewable energy infrastructure, energy transmission and storage in Latin America, Asia and Africa.

Funds raised amounted to 673 million US dollars. Of that, $130 million has been raised in so-called stimulus funding — a security buffer for reducing risks to the private sector — from the governments of Japan, France, and Germany, Total Energy, and philanthropic donors, including the Grantham Environmental Fund. Private investors, shielded from the greatest risks, pledged five times that – $523 million. The Partnership will soon sign its first agreement.

A number of commitments were made at COP27 in Sharm El-Sheikh. As part of a five-year partnership with Kenya, the UK government committed nearly £13 million to new underwriting companies that will reduce risk for investors and are expected to unlock an additional £80 million in climate finance for six energy projects. Agriculture and other sectors. Transport.

The clean energy pillar of Egypt's new Nexus Food, Water and Energy Program has attracted $500 million from international partners, including the United States, Germany and the European Union, to accelerate the adoption of renewable energy in the country.

The financing is expected to unlock at least $10 billion in private investment to install 10 gigawatts of solar and wind power by 2028 and phase out inefficient gas-fired power generation.

At COP 27, the Energy Transition Partnership (JET-P) pledged to mobilize $10 billion in public funds from partner governments to help Indonesia transition away from coal. Private investors joined in the Glasgow Alliance for Net Zero Finance (GFANZ) will raise an additional $10 billion. This was followed in December by the $15.5 billion JET-P program to help Vietnam undermine its goals in matière d'energie propre, the private sector engaging in public financing of $7.75 billion over four years.

An agreement for JET-P worth $8.5 billion for South Africa was announced at COP26 in 2021.

But compared to what's needed, these projects barely scratch the surface. The South Africa Investment Plan, launched a year after the partnership was announced, indicates that $98.7 billion is needed over the next five years to begin the country's transition away from coal. Sources of funding have been identified for about half of this figure.

At least a third is expected to come from private sources, but observers say donor countries are not using the past year to mobilize the level of concessional financing needed to attract the needed private investment. Nor did they address the huge debt piled up by state-run electricity company Eskom, which raised the stakes for investors.

The level of funding is a problem. What is spent is different. Most climate finance projects – about 90% – target mitigation, not adaptation. This is partly because mitigation projects (such as renewables) can generate cash flows to provide returns to investors, whereas adaptation projects generally cannot.

Anjali Vishwamahanan, policy director at the Asian Investors Group on Climate Change (AIGCC), said more innovation, time and effort is needed to develop sustainable and profitable projects.

An example would be building a dam around a lowland, for example with an integrated road project that would generate revenue from road taxes. "We need to bring all stakeholders together, not just private investors, to think about adaptation and sustainability at the system level," said Viswamohanan.

Either way, investors need to think about the physical risks climate change poses to their assets and how to build resilience. AIGCC calls on governments to develop public fiscal strategies to support their national adaptation plans and to bring together private and philanthropic funders with governments and multilateral development banks to identify co-investment opportunities.

Klopp argues that MDBs could easily double or triple their financial commitments from US$140 billion per year and distribute some of the financial leverage to private investors through blended financing.

Small investment centres, which provide loans to governments for public sector projects (such as climate adaptation), currently do not benefit from private sector funding, while institutions such as the International Finance Corporation (part of the World Bank) mobilize private funds for the private sector. Projects don't generate as much investment as they could.

He added that, in the view of most experts, “The Multilateral Development Bank is the most widely used development tool systematically available to the development community.”

Speaking at COP27, Nick Holder, Prudential's chief operating officer for Africa, said he would like to see multilateral and bilateral development banks expand their operations and funding volumes to provide more capital.

“We are definitely looking at greater levels of financial capital, supporting mixed financing solutions that reduce investment risk, not just on a project-by-project basis, but on a larger scale and to facilitate investment and ensure diversification.”

He describes his support for a $14 million solar project in Vietnam as a relatively large undertaking in terms of due diligence and pursuit of certification. "It's a good thing, the right thing to do, but it still can't improve."

In partnership with aid agencies and various private and philanthropic investors, Convergence has developed a Climate Mobilization Action Plan and Sustainable Development Goals to double investment in developing countries to $530 billion. They said the action plan could be implemented within a year and without additional resources from the public sector.

"If we want to invest on a large scale, there has to be a large amount of financing that reduces investment risk…and it has to be allocated to the best examples in the world, wherever they come from." Klopp said.

Most importantly, catalytic funders like CIS need to work together to create a fund large enough to influence climate goals and the Sustainable Development Goals.

USAID, the US government's international development agency working on the plan, has agreed to partner with five Nordic government development agencies to create a financing structure for a $1 billion stimulus for the UAE for the upcoming 28th cycle.

With the approval of the Sharm El-Sheikh Implementation Plan at COP 27, CIS reform is high on the international agenda. climate emergency.”

It also highlights the need for resources in the form of grants, not adjustment loans, for the LDC, which has strong support from the Prime Minister of Barbados, Mia Motley.

Since 2015, Klopp explains, “We have two North Stars, the Paris Agreement and the UN Sustainable Development Goals, which allow us to start really quantifying the amount of investment needed.

One of the major challenges is the system of multilateral development banks and development finance institutions – mandates and legacy processes do not match the speed or scale of the financial commitments and mobilization of private finance required. Their shareholders should point their compass to these northern stars.”

Much hinges on agreeing to chart this new direction at the spring meetings of the International Monetary Fund and World Bank.

The opinions expressed are those of the author. They do not reflect the views of Reuters News, which is committed to integrity, independence and impartiality in accordance with its core principles. Ethical Corporation magazine, part of Reuters Professional, is owned by Thomson Reuters and operates independently from Reuters News.

Angel Mehta

Anjeli Mehta is a science writer with a special interest in the environment and sustainability. He has previously produced current affairs programs for the BBC and holds a PhD in research. @employee

Will the Fed produce a soft landing? | Jeff Snyder and Bob Elliott

A financial expert has branded the ISA, the government's tax-free savings scheme, "pointless" because it only benefits the wealthy.

ESAs are a way for millions of middle-income families to save tax-free interest

Finance expert Paul Lewis told the Resolution Foundation panel that ISAs are the wrong policy because they are "targeted at high earners who don't need extra government help to save".

A report by think tank Resolution Foundation published last Monday found that while the six richest people benefited from tax-free ISAs, those on low incomes or few savers did not.

The think tank recommends an ISA with total tax-free savings of £100,000. All of them."

The panel, which discussed the report presented by Foundation Solution, called on the government to take effective measures to save middle and low income families.

In the first initial payment, automatic opening of accounts for international borrowers is proposed.

The report says Savings Allowance allows basic-rate taxpayers to receive up to £1,000 of tax-free interest on savings, and higher-rate taxpayers £500. But he said the support was "skewed in favor of wealthy investors".

For working-age adults, around £3 in £10 saved in an ISA goes to the top 10% of earners.

The Help to Save scheme is aimed at low-income families who are eligible for benefits, where people can save up to £50 a month and get government help.

But the foundation says take-up of the program is low, with fewer than one in 10 eligible participants taking advantage.

While this suggests the inability of many users to save, those who join the scheme appear to be keen to save as much as possible, with 92 per cent of monthly savings being a maximum of £50, the fund added.

Find out more at Yahoo News UK:

Britain's economic crisis is explained in seven graphs

Martin Lewis warns of 'shocking' 15% rise in broadband bills.

Why 1.4 million UK households are facing a mortgage crisis

The report says Chancellor Jeremy Hunt should review austerity policies and focus on encouraging more people to save.

He said: "Taking the existing schemes together, current policies either do not specifically target harmful spending across all types of ISAs, or there is no scope to significantly expand the distribution of household savings (such as the Enrollment Support Scheme)."

Molly Broome, economist at the Resolution Foundation, said: "Britain is not a country of austerity. The lack of financial stability has left many vulnerable during the cost of living crisis, with households falling into debt and falling behind on paying their bills.

"Government incentives are there to save, but not to such an extent – instead of supporting an increase in the number of people who save, they support tax breaks for people who save a lot."

What is an ISA?

An Individual Savings Account (ISA) is a savings account where you pay no tax on the interest earned.

Each ISA has an annual investment limit.

There are two main types of ISA to choose from, cash only and stocks and shares.

There are other more specialized options.

How to get rich in 2023 with the help of the new revolution of artificial intelligence

The best apps can help you simplify your finances.

It stands out

There are a number of financial apps that will help you manage your money more easily.

These apps can help you budget, reduce credit card debt, invest, and more.

Keeping track of your money doesn't have to be difficult. Fortunately, we live in an age where technology and finance go hand in hand. From budgeting apps to investment trackers, these helpful apps can help you save time and money by helping you make smarter financial decisions. These are some of the best financial apps available today.

1. To set your budget, mint

Mint is the most downloaded personal finance app. It will help you track your expenses, create budgets and create a financial plan. It calculates your net worth in real time and also tracks your credit score. Mint analyzes your spending and provides advice on where you can save the most, helping you find savings you've missed so you can pay off debt faster.

The app lets you create custom alerts, provide updates on your monthly budget, and show your progress toward your financial goals. Among its most important functions is the subscription management and invoice reconciliation service. You can use Mint to waive or negotiate bills on your behalf to lower them. With a 65% success rate, Mint's BillShark has saved members over $2 million.

2. To maximize credit card rewards: MaxRewards

Do you have multiple credit cards? MaxRewards is an app that helps you manage all your credit card points and miles. It can also help you increase your credit card rewards. One of the main features of MaxRewards is to use the best credit card at the stores near you so you can earn maximum rewards for your purchases. You can quickly find the best credit card for each spending category and see all the offers you qualify for. Credit cards often offer additional rewards and offers that you may not be aware of. The app will automatically activate them so you can earn more rewards.

3. To pay off your credit card debt; Next

Tally is a debt settlement app that can save you up to $4,300 over seven years. Tally consolidates all of your monthly credit card bills into one payment, helping you streamline the process of paying off credit card debt. After downloading the app, add your credit cards. Tally then runs a flexible credit check that won't affect your score to see if you qualify for a low interest line of credit from Tally. Once you agree and accept the offer, Tally will immediately pay your cards and you will pay Tally on your monthly invoice. A tally account can be a good option if you can make monthly tally payments and the interest rate offered to you is lower than your credit card interest rates.

4. For active traders: WeBull

WeBull isn't as popular as some of the big names like Robinhood or TD Ameritrade, but the app offers advanced tools and features not found in many other investing apps. Both the app and the desktop version have advanced charting options, powerful validation tools, detailed charts, and dozens of technical indicators, all for free. WeBull has a user-friendly interface and provides access to advanced orders and market data from multiple sources. If you want to trade more actively, WeBull is worth considering.

5. For passive traders, nuts

Acorns is an investment app that makes it easy to invest your excess stocks and ETFs with minimal effort. This is great for those who want to start investing but don't have the time or knowledge. Acorns offers several wallets designed just for you. The app offers different levels of service depending on your needs and offers cash from select retailers, making it a great option for everyone from beginners to seasoned investors.

There is no shortage of financial apps to simplify your finances and make managing your finances easier than ever. Whether you're looking for budgeting tools or automated investment options, there's a program that fits your needs perfectly. Managing your money has never been easier with the right financial apps.

Warning: the highest 0% cash back card we've seen is on sale until 2024.

If you use the wrong credit or debit card, it could cost you a lot of money. Our experts love this great choice, which includes 0% APR until 2024, an incredible 5% APR and all with no annual fee.

In fact, this card is so good that our expert uses it himself. Click here to read our full review for free and apply in just 2 minutes.

MarketWatch Picks has highlighted these products and services because we believe readers will find them useful; MarketWatch News employees were not involved in the creation of this content. Links in this content may earn us a commission, but our referrals are independent of any compensation we receive. to know more

Haley Sachs believes that financing often has a funny and absurd side. Indeed, a sampling of her Instagram account (@mrsdowjones), which has more than 320,000 followers, yields a wide range of posts and memes, including a photo of Kim Kardashian on her private jet: When your budget is avocado toast and iced, coffee is waiting, and suddenly she's private can afford a plane,” and the final clip Sachs exposes is that you can deduct the full value of a Mercedes G Wagon from your business due to an IRS loophole.

Although Sachs comes from a wealthy background—he was born into an Upper East Side family with a father who worked at Goldman Sachs—he says he's always been surrounded by wealth without even realizing it. "My parents were and still are very tight on money," he says. Instead of feeling safe, it left her feeling "helpless, anxious and confused."

So, after she was fired from her $43,000-a-year job — it was a 401(k) — but she said, "Do I need to know what that has to do with it?" remember: In 2019, he launched a digital content business that uses the language of pop culture and memes to explain the basics of personal finance. The company is called Finance is Cool and known on social media as Mrs. Dow Jones has more than 320,000 followers on Instagram, 16,100 on YouTube and 251,400 on TikTok. "I started the business for a younger version of myself," she says.

Some of his most popular writings are about his privileged upbringing. For example, in a recent post, she revealed that she paid $670 to lighten her hair at an Upper East Side salon. Offset the apparent advantage of these expenses by making videos like "Money Rules Only Rich People Know," which include the following six rules:

Don't make so much money. ("Think of money as an asset, but never as a personality trait," he says.)

Know where to spend it and where to save it. ("Always remember, nobody plays 24/7," he says.)

Do not change anything until you use it completely. (When you consciously save for something and then you can buy it, you feel so good and love the product so much that you really want to take care of it, she says.)

Be a little careless with money. (He notes that you want to have money in your life that you can be generous with.)

Confirmed by check. ("If you invite someone somewhere, you're going to have to pay for it," she says, noting that this is true regardless of your gender.)

Be so generous. (Whether it's paying for a cab or buying someone a drink, these small actions really do make a big difference.)

Sachs, who is now a spokesperson for Amex Rewards Checking, also teaches a series of personal finance courses that invite participants to become their own trust funds. And he dreams of starting a production company that will tell great financial stories. "I want to be Mrs. Dow Jones forever," she says. "And I want to bring people with me in the most transparent way." Here are three of the best savings tips he recently shared with MarketWatch Picks.

1. Automate your savings.

"Automation is literally forcing wealth into your future," Sachs said. This means you should set up automatic monthly or even weekly transfers from your checking account to your savings account so you don't have to remember to keep the money.

Sacks prefers high-yield savings accounts that are available somewhere other than the bank statements you regularly open to check your checking account balance. "If you don't see it every day, you forget it," he says. So you save money without thinking or worrying. This works especially well if you have a regular paycheck and a solid budget that allows you to put money away. (See the highest savings rates you can get here.)

2. Wait a week before spraying.

You just saw a great pair of loafers on sale at TheRealReal and you've always wanted them. Of course, they're on consignment, so they've already lost their value, and besides, if you don't buy them, no one else will? Maybe you should take advantage of the offer.

Hang in there, advises Sachs. "Don't rush to buy things you didn't plan on," he says. Most likely, within a week, the urge to click "Buy" will be a thing of the past. If not, use the money you would otherwise spend on something frivolous, like a nice dinner with friends or a new dress for an upcoming wedding.

3. Talk about money.

Sachs thinks you can relate to this story. You've been invited to a bachelorette party this weekend, and your bride wants to book a table at an expensive restaurant every night you're away. You know you can't afford it, but you don't want the hassle, so you go along with it, even if it means paying off high-interest credit card debt.

The way out, Jones says, is simply to hang out with friends. "We live in a culture of watching the Jones family," he says. (You're not included.) "You have to be able to express yourself or you're stuck in this cycle of reactive spending that's harmful."

Be honest in the group message that these types of meals are out of budget and then offer alternative recommendations. For example, a dive bar or barbecue at your rental home with good food and good music. "The more you own what you want and why you're doing it, the better your relationship will be," says Jones.

Gucci Mane & Finesse2Tymes – Gucci Flow [Official Video]

Burgers are the ultimate comfort food for many people, including Mike Puma, who founded the Gotham Burger Social Club in 2013. The concept is simple where a group of burger lovers visit New York in search of the best burger. Almost a decade later, Puma ended his 28-year career on Wall Street to open his own burger shop after successfully building a cult following obsessed with his awesome burgers.

I'll be the first to admit I'm addicted to the next one because I'm a huge fan of these super juicy and crunchy burgers. The first time I had a chance to try one of Puma's famous Gotham Smash burgers (Oklahoma-style fried onion burger with American cheese and onions fried to perfection) was at the 2020 South Beach Wine and Food Festival, right before the pandemic started. Which basically set the standard for every burger I've had since.

Over the past year, Puma has had pop-up after pop-up, with lines enveloping entire blocks, and burger devourers saying it's sometimes worth the 3-hour wait. He reached a turning point where he became less interested in visiting the office where he had been a financial advisor every day for nearly three decades.

“I wasn't that happy. My money customers weren't as excited as the people I gave my burgers to.” “There was a huge difference between being happy because someone is eating my burger for less than $10 and making money from someone on Wall Street, you know, the reaction when I work with clients has never been the same when someone loves the food. The joy and the fact that People's faces are beaming. He's never been so close."

After seeing Puma announce on Instagram (where it has nearly 200,000 followers) that it's coming out of the corporate world and a running burger factory, I knew I had to scramble to get the details.

We chatted about how it all began, the decision to make Burger a full-time business, and what to expect at that first restaurant. Here's how it went:

Amber Love Bond: I've known you for so long I honestly forgot you still had a business job!

Mike Puma: Yes! In October, it was 10 years since I started the Gotham Burger Social Club while working as a financial advisor. There was no "impact" element at the time, I was just doing it for sheer fun and enjoyment. We never thought people would follow what we do. In 2013, terms like influencer didn't exist yet. We only post what we did. If you had told me then we were going to do this interview now? I would like to tell you that this will not happen.

ALB: How did GBSC get started?

MP: I wanted to find the best burger in New York, and one night I posted on Facebook and asked, Who's going on a burger tour? It was a fun way to get my friends together once a month and the response was immediate. Everyone wanted to do it. When we first met we were about 16 or 17 I think and I thought it would be great but in a few months there will probably be two people drinking beer and burgers who will never be produced. It has only grown, as has our social existence, opening up other opportunities.

For most of the early years it was just a group meeting once a month and writing a burger review. But as our audience and presence grew, so did opportunities, and one came from an animal rescue called Social Tees. They reached out and thought it would be fun if we did a burger event together, with the proceeds going to benefit the animals. And I thought it was great! Let's do it! I've always loved Oklahoma-style burgers, so this was an early version of the burger I make now, and it really was the start of who I am today. This led to more ways to cook for people – all fundraisers at the time.

ALB: So the momentum is building!

MP: Yes, and then the epidemic came. But right before that we did Pig 555, which was an aha moment because we had a crazy lineup in that room with all these super chefs. We did something right! Then, around June 2020, bars and restaurants started reaching out to pop-up partners to help them keep their doors open. Some of the locations were on the Lower East Side so I could leave the grill inside (since there is no indoor dining area) and take it outside if needed.

At first I was very limited in what I could do. I didn't have a truck or anything! I relied on UberXL to load my stuff up and get to the grill. Sometimes they saw the grill disassembled and scrapped and I had to find another grill but we made it work. We did three events a week and brought life (responsibly) to New York, which was definitely a dead city back then. We will create these little pockets of life and joy.

People waited 3 hours to get a burger and I was so afraid they would get upset but 99.9% said they would do it again and it was worth it. So we got to the point where we added another grill and more people behind it. We tried to create an atmosphere with music and some excitement.

AL: I love it! You really made these burger lovers happy!

M: Yes! It was nice but I have been practicing both professions for about 2.5 years. You finally realize what you really love to do. A popup requires a lot of work, a lot of coordination, and a lot of hard work. But if we were cooking at minus 25 or 100 on a hot grill, I wouldn't do it any differently. It was so much fun. So, the next step was where to go with this?

ALB: Time to go to the restaurant!

MP: I considered doing both (both jobs) but decided not to in the end. Fundraising and everything together very easily. Now I have a lot of questions about "Are you going to cook?" Would you run in front of the house would you cross the room and say, "Yeah, yeah, yeah, and I'll clean the bathrooms too." You have to work hard to be successful and lead by example. I know it's important to be there and to be the face of the brand because people are used to it and will look for it. We're excited to see where this will lead us.

ALB: Do you live in the Lower East Side neighborhood where you made your temporary home?

MP: The first location would be on the Lower East Side because it makes sense. The neighborhood has been very nice to us and we have a complete crowd. It just feels good. The second location will also be in New York and then we hope to expand outside of New York. I'd rather grow up than grow up too fast.

ALB: Let's talk about the menu! Of course Gotham Smash will be there, but what else can we expect?

MP: We'll keep it very narrow at first. So Gotham Smash is in singles, doubles and trios. We'll also be introducing a grass-fed version of Gotham Smash – it works great and gives people who don't eat beef the chance to get the same experience. We're making my own ode to a bodega classic but in taco form: shredded cheese. It's called the Harlem Taco, and it's a shredded cheese taco with tapatio cream and pickled jalapenos. When I make them sometimes I like them more than a burger! They are amazing!

Then we have sides like fried pickles, french fries, homemade onion rings, baked meatballs, and stuffed meatballs. It will be a set menu for launch, as well as beer and wine – with a full drinks bar due by the end of the year. Hot Dogs, Burger of the Month, and more may appear on the list in the future. It's always fun to try out different flavors and styles.

ALB: As someone who has fled the world, I can't tell you how excited I am for this new adventure for you! There is something very special about having a second job that you find through a passion that brings you so much joy.

MP: I've never seen myself leaving Wall Street, but this experience means a lot to me. People think it's a quick thing, like, "Oh, pandemic, you've been cooking for two years." No, I have been building this brand for over 10 years. I was always excited to see where that might take me, especially as a brand built on social media. I really wanted to see where it would go naturally. I didn't want to swim against the tide at all, but I was glad I could keep up with the tide. And that's what happened here. I got caught, a pandemic hit, restaurants caught fire. It took a long time, especially last year. When people take their first bites, I feel exhilaration unlike anything I feel when I'm sitting behind a computer screen in the office. Although the decision was not easy, it was very easy to make.

For those wondering if Gotham Smash will be back at Burger Bash in Miami and New York, it's on my radar and I can't wait. The Gotham Burger Social Club plans to open its first physical location this spring in New York City.

Top 20 WrestleMania Competitors: Top 10 WWE Specials

Members of the powerful House finance committee blocked a plan by the state Department of Natural Resources to spend $15.5 million on a conservation easement to preserve 56,000 acres of northern Wisconsin forests.

The purchase could be the largest land conservation action in state history, according to Wisconsin Public Radio.

The DNR's policy committee signed the agreement in October, agreeing to spend about $10.8 million in federal forestry assets and about $4 million in state administrative funds on the project.

But state Sen. Mary Felzkowski, a Republican Irma, who sits on the Finance Committee, said Thursday that she and other committee members declined to name their opposition to the use of public money for the project.

People also read…

He told Wisconsin Public Radio that the easement would mean the 56,000 acres would never be developed. He added that there is already a lot of public land in northern Wisconsin, and local governments are concerned about the lack of housing and the availability of land.

"You can't constantly take a property and write it off, deregister it from the private (sector) and write it off from the public," he said. "We cannot afford to continue serving in the north."

Republican lawmakers generally oppose removing private land from tax records.

See Wisconsin State Journal's Favorite Employee Photos of 2022.

Members of the Wisconsin Dells Singers and the Ho-Chunk dance troupe come together for an interactive night of Native American culture on Friday, September 16, 2022, at Glen Park in Madison, Wisconsin. Represented by Madison Parks Division and Ho-Chunk Gaming, the group performed traditional Ho-Chunk songs, stories and dances, interacted with the audience and participated in a question and answer session. John Hart, state newspaper

John Hart State Newspaper

Caitlin Patrick, 14, of Mount Horeb, enters the water on a swing with friends at Stuart Lake County Park on Wednesday, August 10, 2022, in Mount Horeb, Wisconsin. Amber Arnold, state newspaper

amber arnold

Chris Ayers of Madison Window Cleaning enhances views of the Wisconsin State Capitol during a seasonal window cleaning at the AC Hotel in Madison, Wisconsin on Monday, April 11, 2022. John Hart, state newspaper

John Hart State Newspaper

Jim Lorman (right) and his wife Ann Forbes of Madison visit the "CarbonEra Cafe" art installation by Beth Perche and Brenda Baker on the Farm/Art Detour Trail in Prairie du Sac, Wisconsin on Tuesday, October 4. 2022 Amber Arnold, State Daily

State Newspaper Amber Arnold

UW Band Director Corey Pompey leads his musicians during the University Band concert on Friday, April 22, 2022 at the Kohl Center in Madison, Wisconsin. John Hart, state newspaper

John Hart State Newspaper

Governor Tony Evers in the conference room of his office at the Wisconsin State Capitol in Madison on Wednesday, February 9, 2022. Amber Arnold, State Magazine

amber arnold

Spectators at 2022 Foods Lights the Isthmus watch the fireworks close out the event on Saturday, July 2, 2022 at Bryce Stevens Field in Madison, Wisconsin. John Hart, state newspaper

John Hart State Newspaper

Genevieve Buska, left, and Lulu Jaquel, high school seniors at West High School, relax in a hammock during an afternoon visit to Villas Park in Madison, Wisconsin, on Wednesday, May 11, 2022. Amber Arnold, State Daily

amber arnold

Members of the Forward Marching Band, including Junko Yamaguchi, perform in front of an audience at the 2022 Food's Lights the Isthmus Festival at Breece Stevens Field in Madison, Wisconsin. Saturday, July 2, 2022 John Hart, State Newspaper

John Hart State Newspaper

Brinley Crane, 7, of Cottage Grove, reacts to a butterfly that landed on Sun Prairie kindergarten assistant Rhonda Smith while visiting the Olbricht Butterfly Blooms at the Bolz Conservatory in Madison, Wisconsin, on Wednesday, August 3, 2019. 2022. Arnold, state newspaper

amber arnold

Students from the Kickapoo Valley Forestry School in Larforge, Wisconsin, with Finley Thornton in the foreground, cross a road in the Kickapoo Valley Reservation, Wednesday, Jan. 12, 2022. John Hart, state newspaper

John Hart State Newspaper

Monona Grove's Riley Perkins (right) and Kate Walsh celebrate their doubles win against Stoughton. 1st place girls tennis at Stoughton High School in Wisconsin, Wednesday, October 5, 2022. The initials CP on the back of their jerseys are for assistant coach Charles Ping, who collapsed and died while coaching a tennis match. Amber Arnold, state newspaper

State Newspaper Amber Arnold

With sunny skies and slightly warmer temperatures signaling the arrival of spring, a pair of snowmen created from yesterday's snowfall added a wintry touch to Amy Utzig and Jane Schutz's run along the Monona Bay shoreline. near Brittingham Park in Madison, Wisconsin. , April 1, 2022 John Hart, State Daily

John Hart State Newspaper

Spanish and flamenco dancers Tania Tandias (from left to right), Maribel Meyer, Tanya Tanias, Augusta Brula and Andrea Chavez-Lazaro perform in McPike Park at the Shifting Gears Bike Path Dance Festival hosted by the Isthmus Dance Company in Madison, Wisconsin . . , Monday, September 5, 2022 Amber Arnold, State Journal

amber arnold

Martha Siravo shares a moment with her 10-year-old daughter Jazz in her apartment on Monday, August 8, 2022, in Madison, Wisconsin. She is co-founder and president of Madtown Moms and Disability Advocates. Her daughter, who has cerebral palsy and epilepsy, needs cognitive, behavioral, and motor support, will transition to fourth grade, and return to full-time private instruction for the first time since 2020. Martha has been strapped into the Caster chair since 2020. In 2004 , suffered a spinal injury in a car accident. John Hart, state newspaper

John Hart State Newspaper

Monona Grove's Carly McKenzie (right) asks a teammate to come off the bench during a game against Beaver Dam at Northlon Park in Cottage Grove, Wisconsin, on Friday, May 13, 2022. Amber Arnold, State Daily

amber arnold

Members of Madison's aerial dance company Cycropia perform under the branches of an oak tree that is at least 180 years old during rehearsal for a pair of shows at the Orton Park Festival in Madison, Wisconsin. Wednesday, August 24, 2022 Founded in 1989, the group has become a staple of the Marquette Gatherings, with four days of music, food, crafts, and family-friendly activities. This year's program includes the work of 29 participants, including dancers, stagehands, editors and audiovisual technicians. John Hart, state newspaper

John Hart State Newspaper

(Bottom left) Roommates Isabella Bortolotti and Rachel Berder invite friends to their backyard pool party, including Maddie Gering (right), Lola Wojcik (top left) and Grover Bortolotti, all college students who play golf in the summer on the nearby West -Side. Tuesday, June 14, 2022 Madison, Wisconsin Amber Arnold, state newspaper

amber arnold

A traveler enjoys the spring weather while walking along the shores of Lake Michigan on March 16, 2022 in Milwaukee, Wisconsin, as the region experiences its hottest temperatures of the year. John Hart, state newspaper

John Hart State Newspaper

Participants dressed in festive attire ride down State Street toward the Capitol for the Federal Reserve Bank of Wisconsin's Santa Claus Bike Rampage event on Saturday, December 10, 2022 in downtown Madison, Wisconsin. Amber Arnold, state newspaper

State Newspaper Amber Arnold

Wisconsin defenseman Max Clesmith (11), forward Carter Gilmour (14) and defenseman Jacoby No (0) celebrate victory in the second half of the team battle between Brew City and Stanford at American Family Field in Milwaukee, Wisconsin. Friday, November 11, 2022. John Hart, state newspaper

John Hart State Newspaper

Julie Horton of Madison reads "The Otter" from Cynthia Rylant's Family Lighthouse series to her children, Mabel, 5, and Gilbert, 2 (left), while picnicking at Villas Beach on Vingra Lake in Madison. Wisconsin, Wednesday, November 2. 2022. Amber Arnold, State Journal.

State Newspaper Amber Arnold

Students at O'Keeffe Elementary School in Madison, Wisconsin, are photographed during a visit by Wisconsin Governor Tony Evers following his reelection on Wednesday, Nov. 9, 2022. John Hart, state newspaper

John Hart State Newspaper

Marjorie Brisky, 91, watches accordionist Stas Vengelevsky's virtual concert as volunteer Marcel Mertens (right) holds his tablet in Brisky's room at Agress Hospital in Fitchburg, Wisconsin, on Wednesday, December 7, 2022. Amber Arnold , StatePage

State Newspaper Amber Arnold

Jackie Thompson, a preschool teacher at One City School, greets student Hy'Niff Johnson as she arrives for her first day of school on Thursday, September 1, 2022, in Madison, Wisconsin. John Hart, state newspaper

John Hart State Newspaper

Stoughton's Nicolar Rivera turns after defeating Milton's Matt Haldiman in the Division 1 126lb Championship match during the WIAA State Singles Wrestling Tournament on Saturday, February 26, 2022 at the Kohl Center in Madison, Wisconsin . amber lawyer

amber arnold

Amansu Eason and Stacy "Jukebox" Letris perform a dance during Moonshine, a traditional Black History Month performance held in Madison, Wisconsin, on the campus of the UW-Madison School of Dance on Friday, February 25, 2022. , dance and music performances by students, faculty, and alumni of the university's fine arts program. John Hart, state newspaper

John Hart State Newspaper

McFarland's Julia Ackley reacts after breaking 10'6 on her first Division 2 women's pole vault attempt on the final day of the WIAA track meet at Veterans Memorial Stadium in La Crosse, Wisconsin on Saturday, June 4 of 2022. . Amber Arnold, state newspaper

amber arnold

Expecting the birth of their second child in July, Aus Albarguti poses with his wife Maria Zarzalejo during an evening visit to Villa Park in Madison, Wisconsin, Tuesday, May 17, 2022. John Hart, state newspaper

John Hart State Newspaper

Elizabeth Kiko of R&P Kiko Farms in Salem, Ohio, after receiving the Junior Champion at the International Holstein Show award with a yearling winter puppy during the World Dairy Show at the Alliant Energy Center in Madison, Wisconsin. January 3, 2022. Amber Arnold, State Newspaper

State Newspaper Amber Arnold

Visitors enjoy a multimedia experience at Greenway Station in Middleton, Wisconsin during the opening of the Immersive Van Gogh exhibition. Monday, November 28, 2022 with more than 5 million viewers. Debuting in North America in 2020, it offers audiences the chance to "step into" the iconic work of Post-Impressionist painter Vincent van Gogh. Using more than 50 projectors to project images across more than 500,000 square feet, the exhibition features both an original soundtrack and an interpretation of the classics. The fixed obligation will last until January 8. John Hart, state newspaper

John Hart State Newspaper

Mike Mulhaney walks his 9-month-old German Shorthaired Pointer Monty on Tuesday, December 27, 2022, in Belleville, Wisconsin. Amber Arnold, state newspaper

মার্কিন সুপ্রিম রো বনাম পরে বিক্ষোভকারীরা ক্যাপিটলে বিক্ষোভ দেখায়। Tuesday, Friday, February 24, 2022 অ্যাম্বার আর্নল্ড, স্টেট জার্নাল

অ্যাম্বার আর্নল্ড

একটি মৌসুমী সময় এই অঞ্চলে ফিরে ফিরে বেশ মহান উইংরা ক্রিক এর উপকূলরেখা ভাগ নেয় ম্যাডিসন ম্যাডিসন, উইসকনসিনে মঙ্গলবার, 3 মে, 2022-এ হালকা বৃষ্টিপাত ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। ।।।।।।। জন হার্ট, স্টেট জার্নাল

The word "fintech" has dominated tech stocks in recent years. From crowdfunding to customer growth, product launches to scandals, the new game changers are everywhere in consumer banking, credit, payments, investing and cryptocurrencies.

You have good reason to think we have reached the pinnacle of fintech.

But the areas where most fintechs focus today represent only a small fraction of the $23 trillion global financial services market. Products like Cash App, Robinhood, and Chime operate in markets that are intuitive to the average consumer, but consumers are only seeing the tip of the iceberg.

The next wave of fintechs will focus on increasing lesser-known and less "sexy" markets that are critical to the global economy, and one of the biggest markets poised to experience disruption is agricultural finance. 2022 has seen a quiet but steady rise in fintech products made for mass farming, and it's just getting started.

Why offset agriculture in the first place? In the technology sector, for two main reasons: the size of the market and the limitations of existing service providers.

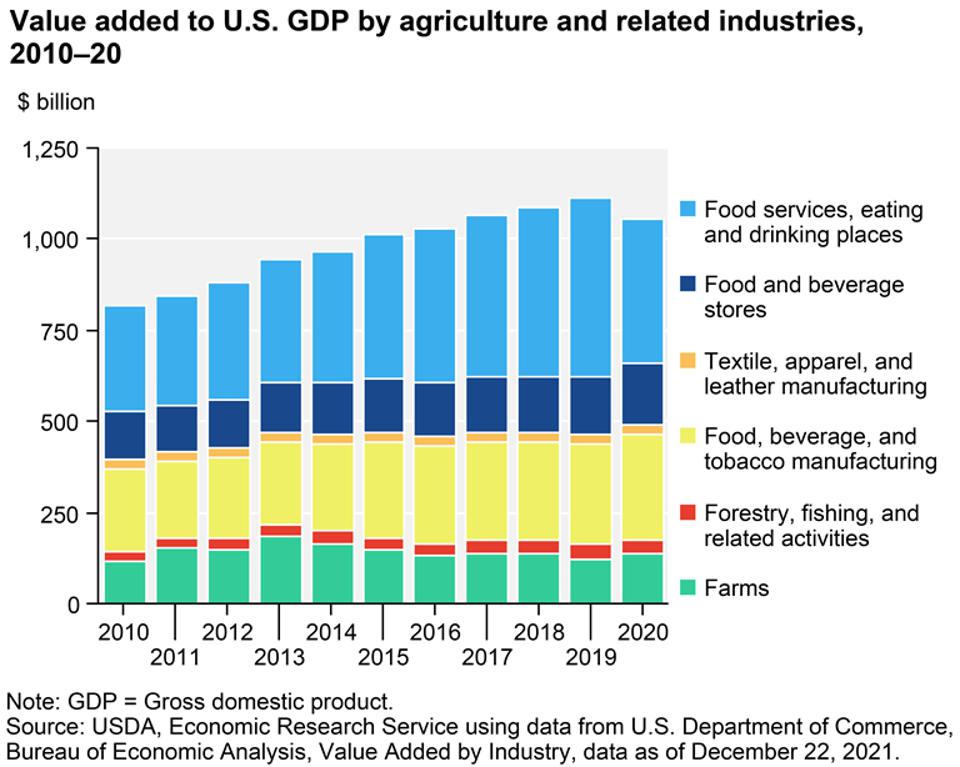

Looking at the United States alone, while agriculture contributed $134.7 billion to GDP in 2020, industries that depend on agriculture — food manufacturing, food service, textiles — contribute more than $1 trillion annually. economy, which contributes more than 5% to the annual GDP. For many developing countries, the share of agriculture in the total economy is much higher, in some countries as high as 25%.

However, financial services are not as competitive as one would expect in a sector as large as agriculture. Looking back at the US market, which is one of the best in terms of farm finance, farm debt has risen steadily over the past year, farm loan interest rates have risen sharply, and farm loans have continued to grow, while the number of Agricultural banks targeting banks remained down.

Enter fintech.

In a world where demand for food will grow 70% by 2050, requiring an annual investment of $80 billion, slow incumbents create huge opportunities for new entrants.

While “agricultural finance” refers to a broad and diverse set of activities – equipment lending, supply chain finance, commodity trading, agribusiness banking – emerging fintech companies focus on a variety of sub-sectors;

Agricultural loans. England's Oxbury Bank double-funded £650m in farm loans to British farmers last year. Tarfin in Turkey and Agro.Club in Eastern Europe provide supply chain finance to medium-sized farmers, who usually have to turn to agricultural suppliers for loans at exorbitant interest rates. Companies like Crowde in Indonesia and Campo Capital in Brazil have built a network of agricultural loan partners. Players like Traive, AgroLend, Terra MONTH3: Magna and Agree are involved in livestock loans in Latin America. ProducePay allows Mexican farmers to take out loans against collateral from their American buyers.

Agricultural payments. Agriculture tends to lag behind in adopting new payment methods, as transactional products such as checks still account for 90% of the industry. Bushel recently launched an integrated payment gateway, digital wallet and payment functionality that connects shoppers to 40% of US grain suppliers.

Product prices and commercial data. Deep markets in grain, livestock and other commodities are critical to a well-functioning agricultural supply chain, and accurate price data is the lifeblood of this sector. This market allows buyers to protect themselves from rising food prices and large agribusinesses to protect themselves from price fluctuations in the supply chain. FarmLead specializes in digitally connecting grain trading networks and integrating trade data into other digital tools for grain growers and buyers.

Insurance: Agriculture is the most balanced sector in terms of climate change-related risks from droughts, floods and natural disasters. Insurance is essential to prevent the collapse of a fragile agricultural system, but traditional insurance companies are struggling to cover agricultural insurance. This is where platforms like World Cover, which offers satellite climate insurance to small farmers in countries like Ghana, Uganda and Kenya, or GramCover, which focuses on access to insurance for farmers in India, come into play.

Market . While ecommerce platforms like Shopify have opened up global retail marketplaces to independent sellers, most farmers markets still operate as centralized offline exchanges. In Kenya, startups such as Twiga Foods, FarmShine, ShambaPride and M-Farm have set up platforms to directly connect farmers with buyers and publish easily accessible pricing information.

Banking. The biggest earners for fintech companies are acquiring new customers, such as loans or insurance, and cross-selling banking products tailored to their specific needs. DeHaat provides financial services to farmers in India in the fields of credit, procurement, advisory and sales. New Zealand data provides financial planning tools for farmers. FarmDrive creates a credit score for Kenyan farmers. Seso provides recruiting, workforce, and asset management tools to streamline payroll in US agriculture.

Over the next decade, we will see the development of parallel markets for fintech products across all categories: banking, loans, savings, payments, investments, HR, payroll and trading, with a particular focus on agriculture.

While agriculture may not be the most obvious market for fintech, it is certainly one of the largest and most productive, and I expect many of these companies to thrive and dominate the next wave of fintech.

2017 Albright – Victoria White – Financial inclusion and the FinTech revolution